Ocean rates show surprising early summer bounce

Spot rates published by Freightos to move 40-foot containers from China to the U.S. West Coast and from China to the U.S. East Coast are shown in white and red, respectively. (Chart: SONAR)

To the surprise of many, ocean spot rates are approaching, or have risen beyond, February peaks, which coincided with the start of the Red Sea attacks. This CNBC article outlined what’s changed in recent weeks to exacerbate the lingering impacts of the Red Sea situation, including a combination of adverse weather in Asia, seasonal strength and an emerging shortage of oceangoing containers.

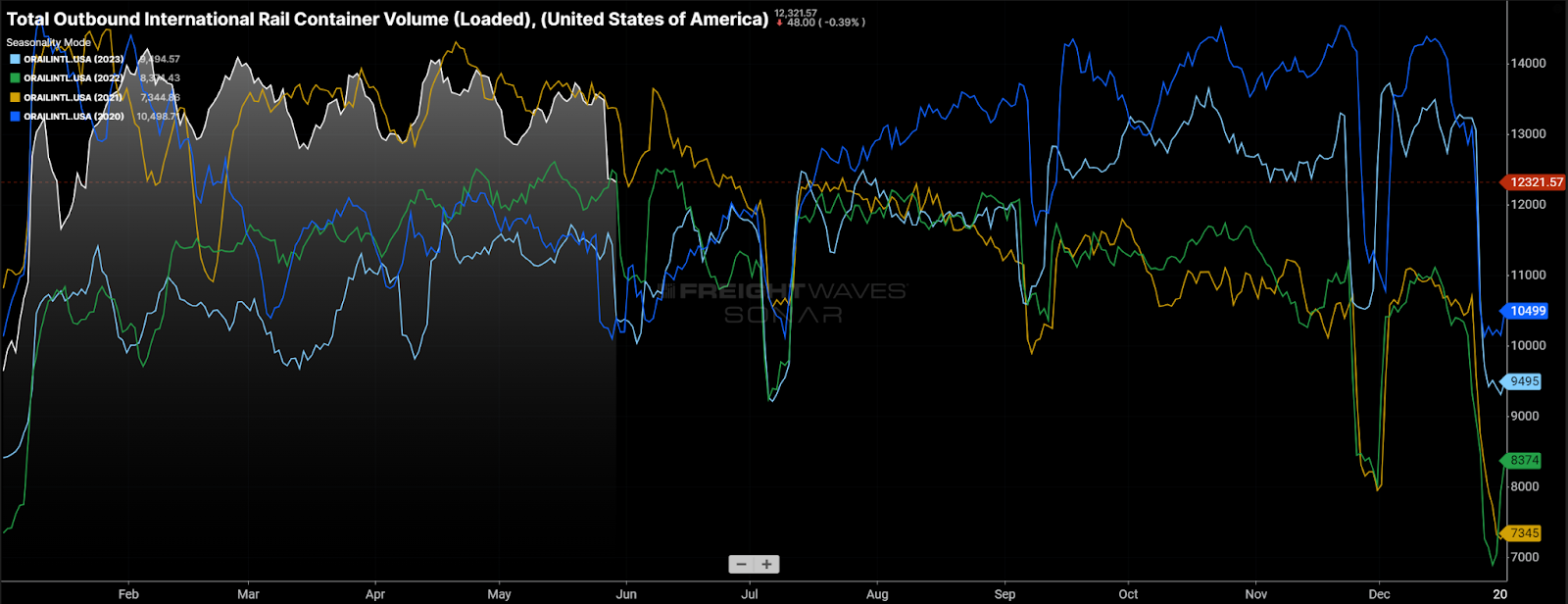

I expect that last point — recent availability issues of oceangoing containers — to have an impact on the North American intermodal industry and the degree of transloading from international/oceangoing containers into 53-foot domestic containers.

Loaded international intermodal volume. Going forward, international intermodal volume may be impaired by emerging container availability issues. (Chart: SONAR — ORAILINTL.USA)

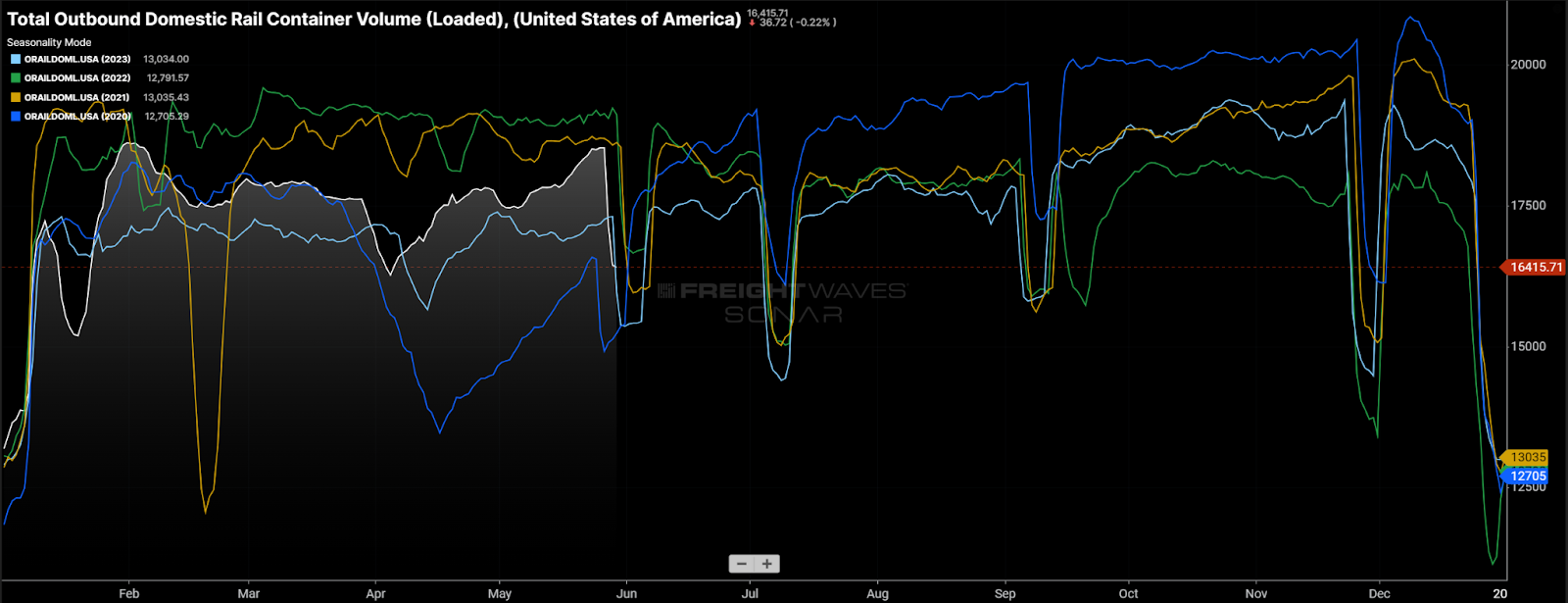

Year to date, the increase in international intermodal volume has been the primary driver of overall increases in intermodal volume. This year, SONAR shows that loaded international intermodal volume is up 24% y/y while loaded containerized domestic intermodal volume is up 3.5 y/y. That appears to be changing with domestic intermodal volume 3% higher in the first 30 days of May compared to the 30 days of April.

For shippers, that may mean less availability of the lower-cost (and lower-service) international intermodal option. The trend stands to benefit the domestic intermodal carriers (e.g., J.B. Hunt, Hub Group and Schneider), which participate in the domestic intermodal market.

Loaded domestic containerized intermodal volume, which picked up steam in May. (Chart: SONAR — ORAILDOML.USA)

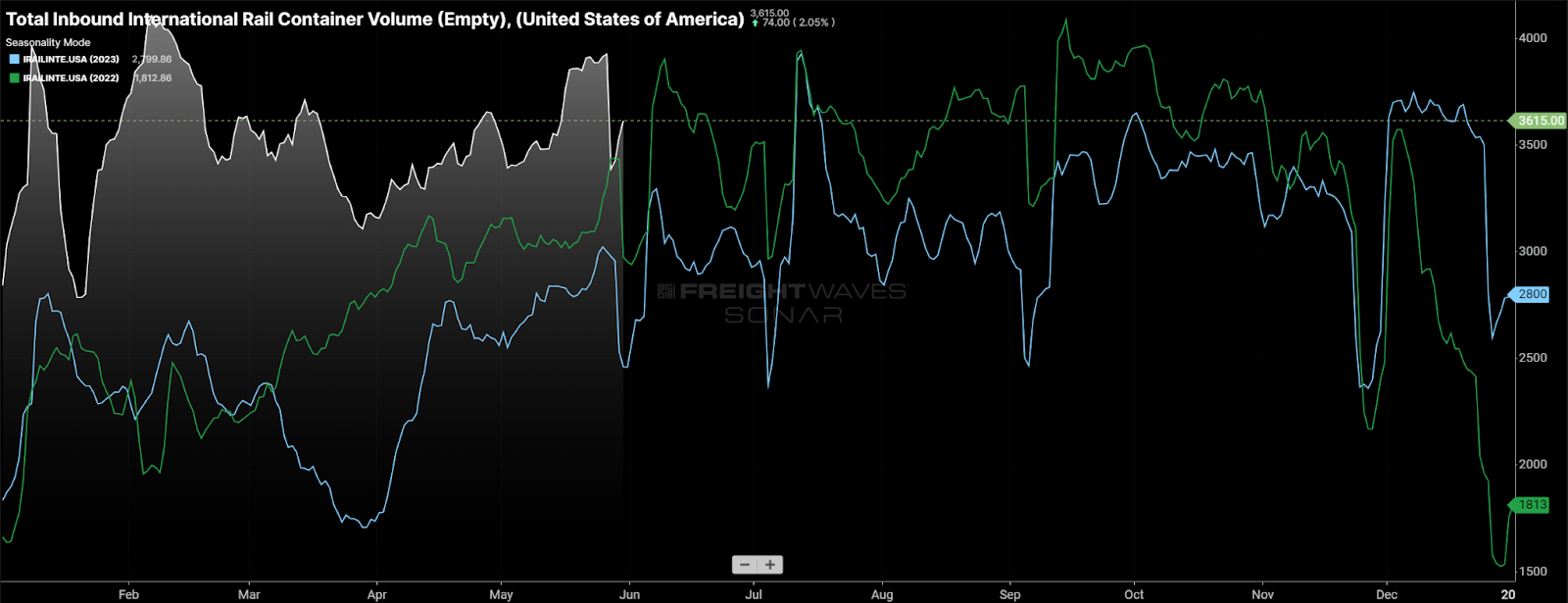

Due to this year’s growth in international intermodal volume, the volume of empty international containers repositioned exceeded 2022 and 2023 levels by 33% and 47%, respectively. A shortage of international containers would cause this metric to decline as container ship lines become less willing to send large volumes of containers inland. (Chart: SONAR — IRAILINTE.USA)

Publicly traded carriers become more bullish

Tender rejection rates moved more in response to International Roadcheck and Memorial Day than they did last year, a sign that freight markets are closer to equilibrium. (Chart: SONAR)

I recommend Todd Maiden’s recent article, which has highlights from a Wall Street conference. What’s surprising is that carriers are not far removed from their first-quarter earnings calls, which mostly took place in mid- to late April but struck a more optimistic tone in May. Highlights from Maiden’s article include:

Werner CEO Derek Leathers says the company is seeing less pressure from shippers to reduce rates and is also seeing a decline in customer churn and improved bid compliance.

Leathers said some price renewals have moved higher, but that is not true across the board.

Werner’s pricing is mixed across segments: Pricing in its one-way segment will be down 3%-6%, while pricing in the dedicated segment, which counts discount retailers as customers, is flat to up 3%.

Schneider CEO Mark Rourke said his company has captured low-single-digit price increases on contract renewals in its one-way truckload business.

CPG companies should be auditing fees imposed on them by retailers

CPG companies that are regularly charged significant fees by their retail partners will want to read this article by Grace Sharkey. Cambridge Capital, a supply chain-focused investment firm, announced last Wednesday that it made a majority investment in retail auditing software Stat Recovery. Stat found that over 50% of compliance deductions imposed on suppliers by retailers are driven by retailers’ errors rather than suppliers’ errors. The software provider is expanding from food/beverage to other CPG verticals.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.

")