Capacity already stretched thin by Red Sea diversions is combining with an unexpected increase in demand in recent weeks to send ocean container spot rates spiking, and pose familiar challenges to shippers with long-term contracts, making rate visibility and market intelligence even more important to decision-making than usual.

Carrier adjustments due to Red Sea diversions for the most part succeeded in keeping containers moving on schedule through March and April. But alongside the success were gradual signs that carriers were falling behind: pockets of congestion developed due to increases in port omissions, delays and missed departures alongside a decrease in empty containers at export hubs as well.

With demand stable in those months though, carriers still had just enough capacity and equipment to keep the market balanced and rates elevated but level.

But things started to change dramatically in May.

Demand for ocean freight out of Asia unexpectedly picked up early in the month reflecting the possible start of restocking in Europe and an early peak season on the transpacific due to concerns over Red Sea or labor-driven delays later in the year. As a result congestion began to worsen and the supply side deficits began to be felt as empty container shortages in Asia and spiking rates.

Access Spot Rates – Updated Daily

Renegotiate With Confidence and Get the Best Quote

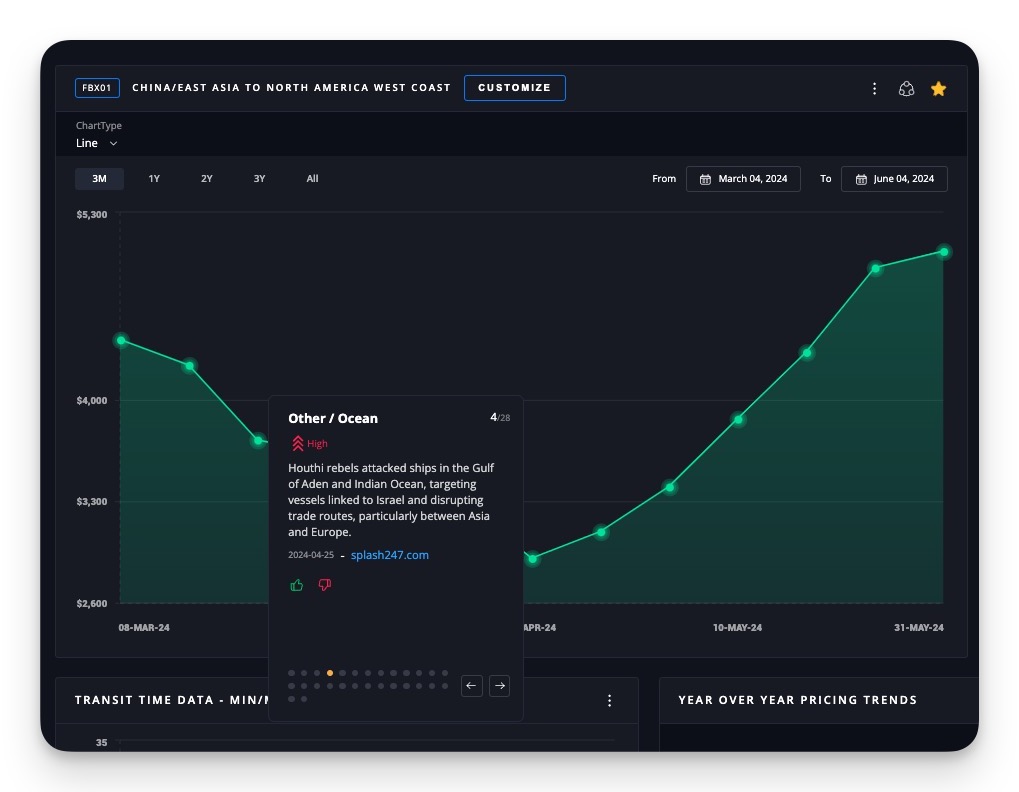

Since the end of April, Asia – N. America West Coast spot rates, for example, have spiked more than 70%, passing the $5,000/FEU mark and their previous 2024 high hit in February when prices first soared on the start of Red Sea diversions.

With capacity and equipment scarce and spot rates now several thousand dollars above long-term contract levels, annual agreements are once again becoming unreliable.

A recent Freightos Group survey of more than fifty logistics professionals found that since early May, nearly 70% of BCOs and forwarders with long term ocean contracts have had containers rolled or pushed to the spot market, or are facing contract renegotiations with carriers to increase their long term rate levels.

And there’s uncertainty as to how long this will last: Many (40%) think that the situation will improve within the next two months, while 26% expect these types of disruptions to last until peak season ends and another 22% do not expect conditions to improve much until Red Sea traffic resumes.

With so much in flux, rate visibility and market intelligence are even more important than usual – especially for BCOs and forwarders facing contract instability and tough decisions like when and how much to shift to spot, or the acceptable level for a renegotiated contract.

Learn more about Freightos Terminal here.

")