Demand for air cargo has continued to be strong around the globe throughout the second quarter, Q2.

The International Air Transport Association (IATA), the global trade association representing airlines, have released statistics for global air cargo markets, which display a strong annual growth in demand into the second quarter (Q2).

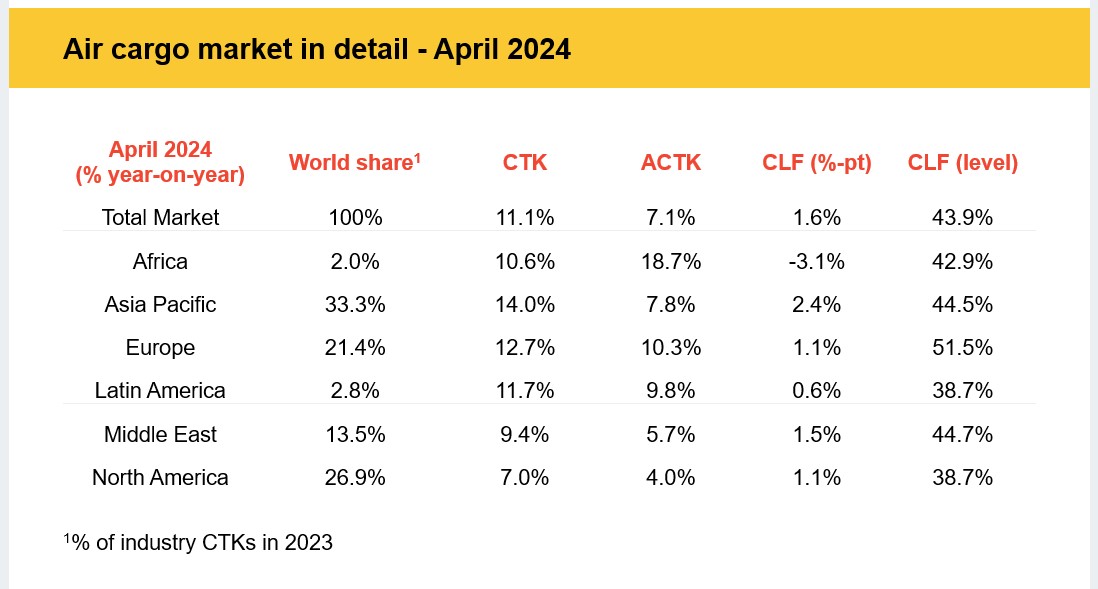

The total demand, which is measured in cargo tonne-kilometres (CTKs*), has risen by 11.1% compared to April 2023 levels (11.6% for international operations). This double-digit year-on-year growth has occurred for a fifth consecutive month.

The capacity, which is measured in available cargo tonne-kilometres (ACTKs), has increased by 7.1% compared to April 2023 (10.2% for international operations).

Credit: IATA

“Air cargo demand started Q2 with a solid 11.1% increase. While many economic uncertainties remain, it appears that the roots of air cargo’s strong performance are deepening. In recent months, air cargo demand grew even when the Purchasing Managers Index (PMI) was indicating the potential for contraction. With the PMI now indicating growth, the prospects for continued strong demand are even more robust,” said Willie Walsh, IATA’s Director General.

Several factors in the operating environment should be noted:

• In April, the PMIs for global manufacturing output and new export orders turned positive (51.5 and 50.5 respectively). This is the first time in two years that the new export orders PMI has been in growth territory.

• Industrial production increased by 1.6% in March year-on-year, while global cross-border trade contracted by 0.8%.

• Inflation remained relatively stable across the US, EU, and Japan in April with rates at 3.4%, 2.6%, and 2.5%, respectively. China reported a 0.2% increase in consumer prices year-on-year—a positive signal amid concerns over China’s economic slowdown.

Credit: IATA

April Regional Performance

Asia-Pacific airlines saw 14.0% year-on-year demand growth for air cargo in April – the strongest of all regions. Demand within the Asia market grew by 13.2% compared to April 2023, and the Asia-Europe route grew by 17.7%. The Middle East-Asia route rose by 10.4%, 9.5 percentage points (ppt) less than the growth recorded in March. Capacity increased by 7.8% year-on-year.

North American carriers saw 7.0% year-on-year demand growth for air cargo in April —the weakest among all regions. Demand on the Asia-North America trade lane grew by 7.3% year-on-year, while the North America-Europe route saw an increase of 5.6%, marking the largest demand growth for this route since September 2022. April capacity increased by 4.0% year-on-year.

European carriers saw 12.7% year-on-year demand growth for air cargo in April. Intra-European air cargo rose by 34.4% compared to April 2023, reflecting the highest annual growth in over a decade and a jump of 8.1ppt compared to the month before. Europe–Middle East routes saw demand increase by 30.1%, experiencing a drop of 8.5ppt compared to the previous month’s figure. April capacity increased 10.3% year-on-year.

Middle Eastern carriers saw 9.4% year-on-year demand growth for air cargo in April. The Middle East–Europe market performed particularly well with 30.1% annual growth, ahead of Middle East-Asia which grew by 10.4% year-on-year. April capacity increased 5.7% year-on-year.

Latin American carriers saw 11.7% year-on-year demand growth for air cargo in April. Capacity increased 9.8% year-on-year.

African airlines saw 10.6% year-on-year demand growth for air cargo in April. Demand on the Africa–Asia market increased by 25.8% compared to April 2023. April capacity increased by 18.7% year-on-year.

More Like This

")